HAL Trust | Greatly undervalued Dutch holding company

Why we think you can buy this business with a high margin of safety...

What is HAL Trust?

HAL Trust is a Dutch holding company with a focus on long-term value creation through strategic investments. The firm owns stakes in roughly 30 companies, spanning various industries, with a particular emphasis on maritime (sea-related) services.

The two flagship companies in HAL's portfolio are:

Boskalis: specializes in dredging and offshore energy.

Vopak: manages terminals for oil and gas storage.

Boskalis

Boskalis is HAL’s crown jewel and the world’s leader in dredging. It generates over half of HAL’s revenue and net profit. Beyond dredging, Boskalis is a major player in offshore energy, handling complex projects like building oil platforms and offshore wind farms.

Scale: Operates a fleet of 500+ vessels specialized for challenging marine tasks.

Value: Book value set at €4.4 billion, representing ~30% of HAL's total book value.

Why you should care: Investing in HAL Trust is essentially a 50% bet on Boskalis. If Boskalis struggles, HAL Trust’s performance will likely follow. It’s comparable to investing in Prosus, which is heavily tied to its 25% stake in Tencent.

Vopak

Vopak, another key holding, is the world’s largest independent terminal owner, strategically located in major ports like Rotterdam, Los Angeles, and Shanghai.

Focus: Stores oil, gas, chemicals, and new energy solutions like LNG and CO2.

Profitability: Delivers very high net profit margins of over 30%.

Did you know? Vopak has been in business for over 400 years—dating back to the 17th century (1616 to be exact) when it started as a Dutch trading company. Its longevity and resilience make it one of the oldest companies in the energy storage industry today.

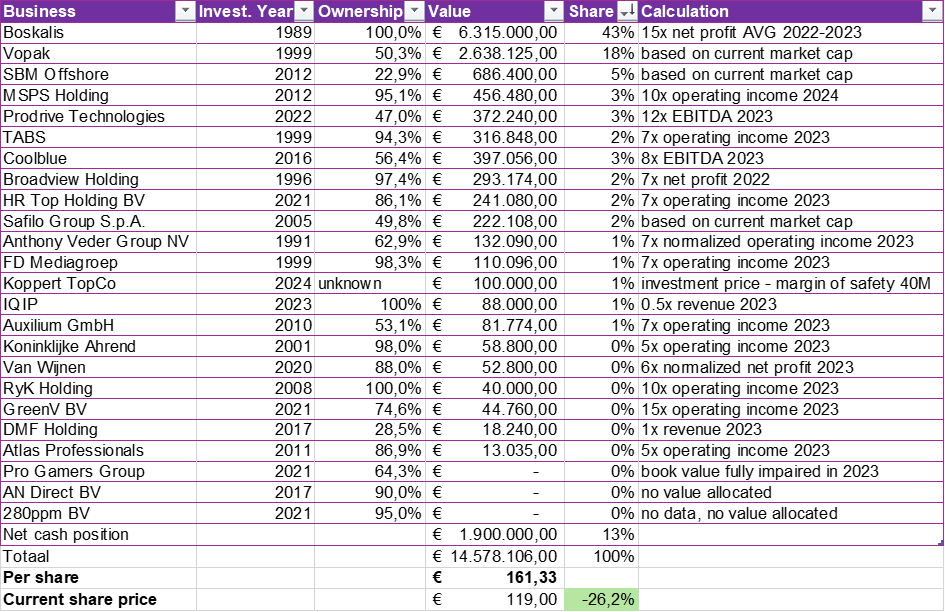

HAL’s value lies in its strategic stakes across multiple companies, combining majority and minority holdings. Using conservative valuations:

Sum of the parts

HAL values Boskalis at €4.4 billion, making up nearly 30% of HAL's book value. But I believe it's worth more.

Here’s why:

They are market leaders and dominate in dredging and offshore energy.

Climate change and adaptation are areas where Boskalis can greatly assist governments, all over the world.

DEME (A Boskalis competitor) trades at 25x earnings. I’m using 15x on Boskalis’ average profit for 2022 and 2023, as it hit peak earnings in 2023.

Keep in mind, though, Boskalis remains a cyclical business.

I multiplied HAL's stake by market value for Vopak, SBM Offshore, and Safilo. For less transparent holdings, I applied conservative estimates.

If you believe the assumptions above, then HAL is currently undervalued by 26%. You can also look at the equity per share of HAL, which is around €150. Based on this, HAL is about 21% undervalued.

Are you interested, and do you want to read our full analysis of HAL? Our premium members have now access through our premium platform at www.thedutchinvestors.com!

how does the shareholder structure look like in HAL?

What's your reason to ignore HAL's holding in Technip Energies ?