3 Undervalued Small Caps

3 small caps that seem undervalued: Why we like them.

Small-cap stocks typically range from $250 million to $2 billion in market cap and offer individual investors a unique edge over hedge funds and large investment firms.

The small caps we handpicked for you:

Nedap: Dutch small cap that is transforming from a hardware to a software company with recurring revenue.

EVS: A mission-critical broadcasting company that is building an ecosystem for its customers.

Greggs: The most popular fast-food chain in the UK.

Many institutional investors avoid small caps due to liquidity constraints. This means less analyst coverage and more potential for mispricings that could lead to undervaluations. Because of this, small caps present a golden opportunity for investors like you and me!

If I were working with small amount of money, it would just open up thousands of possibilities to me - Warren Buffett

Of course, like everything in life, there are some risks to consider, such as less information available (can also be an opportunity), higher volatility (can also be an opportunity) and, usually, weaker financial stability, since they’re competing with bigger players.

When you weigh the risks against the upside potential, small caps can be an exciting hunting ground for investors who do their homework. That’s why we’ve handpicked three of our favorite small-cap stocks that we believe are undervalued.

Disclaimer: the undervaluation is just our own opinion. Always do your own research.

Small Cap 1: Nedap

💰 Market cap: €388.00M

🏢 Sector: Technology (Information services)

⚙️ Founded: 1929

🌍 Country: The Netherlands

Why we like Nedap

If you are not Dutch, you've probably never heard of Nedap. Nedap is a Dutch software/hardware company, worth around €400 million and is listed on the Amsterdam Stock Exchange.

Nedap is transitioning from a hardware to a software-driven company, prioritizing recurring revenue. Since this shift began, recurring revenue has grown at a 17% CAGR (2019–2023) and now accounts for 40% of total revenue.

Yet, we believe the market still values Nedap as a traditional hardware business, overlooking its software-driven business model.

Helping you understand Nedap

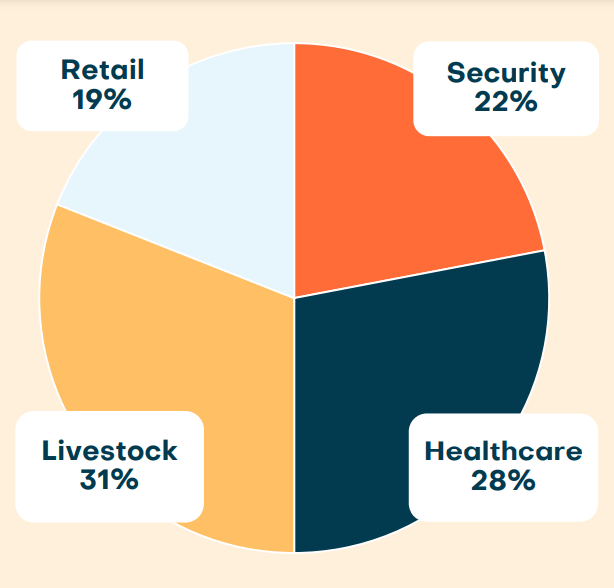

Nedap aims to dominate four key markets: Security, Healthcare, Livestock, and Retail. Here's how revenue is distributed:

When you look at the 10-year revenue and EPS figures, you might think it’s a slow-growing company, and to be fair, it was. But since transitioning, the revenue has re-accelerated to 8.6% 3-year CAGR. Profits are also growing faster than revenue, something we love to see.

Nedap's management believes it can be the market leader in the chosen focus areas above.

Livestock Management - 31% of revenue

Nedap’s CowControl and Milking Control systems track millions of cows across 30.000 farms and has 40% global market share. Farmers don’t just buy a product; they integrate their entire workflow into Nedap’s ecosystem, monitoring fertility, disease detection, milk yield, and feed control. Think of it as a Fitbit for cows. Switching means retraining staff, recalibrating operations, and potentially risking months of lost productivity.

Healthcare - 28% of revenue

Nedap’s "Ons" platform powers administrative workflows for thousands of Dutch healthcare institutions, commanding 60% market share in elderly care and 50% in disability care (M&I Partners). With a 99% retention rate, hospitals and caregivers deeply rely on its seamless integration with patient records, financial systems, and logistics. The switching costs are immense, making it one of Nedap’s strongest segments.

Security - 22% of revenue

The security division follows the same pattern. Especially in Europe, Nedap has a strong market position with 36% of the top 250 European organizations as a client. These clients include Airbus, Vodafone, Volkswagen and Unilever. Worldwide, 2.500 organizations are making use of Nedap’s security solutions.

Its PIAM (Physical Identity & Access Management) is deeply embedded into HR systems, dynamically adjusting access rights based on employee roles. The complexity and regulatory requirements of access management make switching a massive logistical challenge, requiring months of testing and implementation, deterring any potential migration to another provider.

Retail - 19% of revenue

In retail, Nedap’s iD Cloud platform dominates RFID-based inventory management, increasing accuracy from an industry average of 70% to an unrivaled 99%. It’s the inventory management platform for global retailers like Adidas, Puma, Foot Locker, Boss, Decathlon and many more. It synchronizes supply chains, improves loss prevention, and powers omnichannel operations. Transitioning to another system would require re-tagging every product, retraining staff, and risking costly inventory mismanagement.

Do we own shares in Nedap?

Yes, all four of us do. Now that you know Nedap a little better, you might see why Nedap is included in all four of us their personal portfolios.

Because we’re passionate about this Dutch small cap (and a little proud of our home country 😉), we’re giving you free access to our full analysis. Just subscribe below to unlock the premium Nedap report!

Already subscribed? Request the analysis here.

Please enjoy the Nedap analysis.

Small Cap 2: EVS

💰 Market cap: €483.53M

🏢 Sector: Technology (Communication equipment)

⚙️ Founded: 1994

🌍 Country: Belgium

Why we like EVS

EVS Broadcast Equipment is a mission-critical company that is essential for live broadcasting. EVS broadcasts big events like the Olympics, Champions League and European Championships.

Take the Champions League Final for instance: it’s filmed with 42 cameras, each generating 1 to 10 GB of data per second.

All these recordings need to be combined into a single broadcast, and that’s where EVS, a Belgian small-cap company, comes in.

Over the past five years, the company has achieved a revenue CAGR of 10%, yet it’s currently trading at just 12 times earnings. In 2023, revenue (excluding major events) even grew by 25%.

After facing challenges and increased competition, EVS is back on track under CEO Serge Van Herck, with a clear strategy for growth and innovation. Even though we are not invested in EVS yet, the company is high on our watchlist.

Helping you understand EVS’s moat

If you've watched a football match, chances are every replay, slow-motion shot, and referee review was powered by EVS. Its LiveCeption platform is the gold standard, commanding an estimated 30% market share in sports replays.

In sports broadcasting, where rights are worth millions, advertisers invest heavily, and fans are deeply invested, reliability is absolutely a must have. Cutting corners on equipment is not an option, making EVS’s offerings mission-critical.

Just as Adobe is the standard software for graphic designers, EVS is the industry standard for broadcast operators.

Operating EVS equipment requires specialized training, meaning switching isn’t just difficult, it’s impractical. Because EVS is the standard, broadcasters seek EVS-trained operators. This is driving more professionals to learn the system, reinforcing EVS’s position in the industry.

Our analyst Luuk already wrote this article on EVS, for those who want to go deeper:

Premium members have access to the full analysis on the TDI Premium Platform.

Small Cap 3: Greggs

💰 Market cap: £1.93B

🏢 Sector: Consumer cyclical (Restaurants)

⚙️ Founded: 1939

🌍 Country: The United Kingdom

Why we like Greggs

Greggs is the UK’s largest and most beloved fast-food bakery chain, specializing in sandwiches, pastries, and coffee. Known for its iconic (vegan) sausage roll, Greggs operates under the motto: “Convenient and Cheap.”

With 2,500 stores across the UK, Greggs has more locations than McDonald’s and Starbucks combined in the UK. Yet despite its dominance, the stock trades at just 13 times earnings. This while Greggs has by far the strongest moat among its peers in the UK:

Brand power: According to Statista, Greggs is the most popular restaurant chain in the UK, scoring 79% approval, well ahead of McDonald’s (58%).

Lowest cost provide: Greggs is the most affordable fast-food option in the country, making the company resistant during crises.

Because we don’t have any Greggs stores in The Netherlands, our analyst Siem went to London to visit the stores himself.

What investors are overlooking in Greggs

We believe investors are too short-term focused and not willing to wait until 2027 when we expect a significant increase in free cash flow of Greggs.

Since 2022 Greggs have increased their CapEx spendings significantly, investing in distribution centers enhance their efficiency.

After 2027, CapEx is expected to decrease to 5% of revenues. This will result in an expected free cash flow in the range of £240 million. Considering the current stock price, that would mean you only pay 8 times free cash flow in 2027 for a quality company like Greggs.

Because Greggs has a ROCE of 20%, a strong moat, reliable management and proven business model, we expect these investments to pay of well.

While the market is worrying about the next quarter and inflation, we’re thinking about the free cash flows of Greggs in 2027 and beyond. This is why we believe Greggs is presenting an interesting opportunity at its current valuation.

Free access to the premium Nedap analysis?

Now that we’ve shared three undervalued small caps with you, we’d like to give you full access to the analysis of the only small cap all four of us personally own: Nedap.

Subscribe below, and we’ll send you our premium Nedap analysis as a welcome gift in your inbox 🎁. You won’t need any further sign-up to access the analysis.

Already subscribed? Request the analysis here.

Of course, you can’t blindly invest in these companies based on this article. You always need to do your own research. We sincerely hope we were able to introduce you to three interesting small caps in this article.

We look forward to introduce you to many similar companies in the future.

Have a wonderful day and happy investing.

The Dutch Investors.

Great analysis, Dutch!!! (specially about Greggs)

Thanks for highlighting these.