The PayPal Problem

We did a deep dive into PayPal, and this is the problem we found.

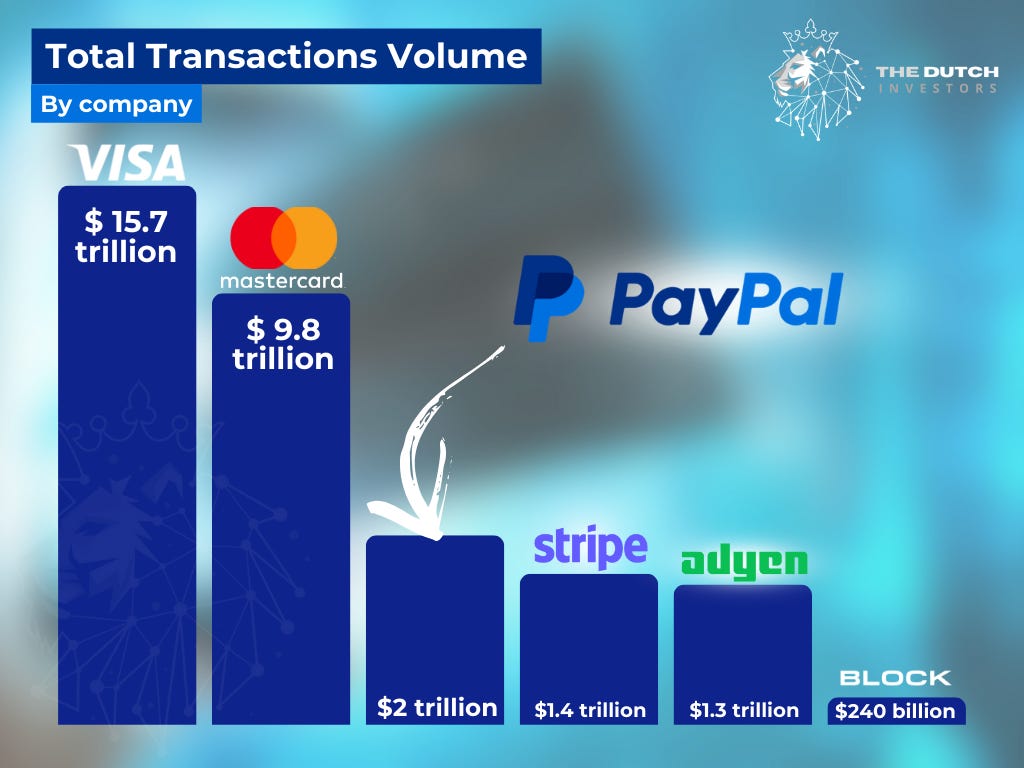

PayPal, who doesn’t know the company? PYPL 0.00%↑ really doesn’t need an introduction. With over 430 million users and nearly $2 trillion in transaction volume, it is no small player.

To put that in perspective, the other players PayPal competes with include Adyen, Stripe, Block, Worldpay, and others. Moreover, they are enormously dependent on the most powerful players in this market: V 0.00%↑ and MA 0.00%↑.

We have a love–hate relationship with PayPal. We are very familiar with the platform, its features, strengths, and limitations. We use it ourselves alongside Stripe. As a result, beyond analyzing the company from the outside, we have a front-row seat when it comes to comparing features and overall developer experience. While PayPal/Braintree works well, our preference leans clearly toward Stripe.

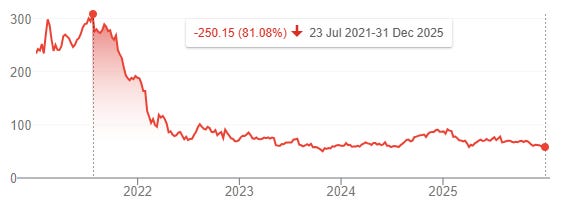

It would be an understatement to say that PayPal hasn’t been doing too well. The company is down more than 80% from its peak.

Why? What problems are they running into? Are these structural issues, or can they be solved? What is needed to turn the tide? These are the questions that must be answered to come to a decision on whether to buy, add, or sell.

What’s the problem?

There are several issues PayPal is facing. If you ask us, we think it comes down to these:

Apple Pay and Google Pay utilize hardware-level biometrics to offer a frictionless checkout experience that PayPal’s app-based login cannot structurally match, leading to market share erosion among younger demographics.

PayPal does not own the underlying payment rails and must pay nearly half its revenue to Visa and Mastercard, capping its profit potential and leaving it vulnerable to partner fee hikes.

While total payment volume grew, profits did not keep pace because the growth came from low-margin backend processing (Braintree) rather than the profitable checkout button. This unbranded Braintree division faces a race to the bottom on pricing against technically superior rivals like Stripe and Adyen, causing PayPal’s overall profit margins to decline even as volume grows.

A history of acquisitions has left PayPal with a Frankenstein stack of disjointed legacy systems that slows down innovation velocity and bloats maintenance costs compared to unified competitors.

Investors lost faith and confidence in management when they were trying to build a WeChat-like ‘super-app.’ As you can imagine, this did not come to fruition. Moreover, after forecasting 750 million users by 2021, active accounts stalled at ~430 million, leading the market to conclude the platform has reached total saturation.

Major ecosystem gatekeepers like Amazon and Shopify actively prioritize their own checkout solutions or exclude PayPal entirely, effectively locking the company out of significant segments of e-commerce growth.

Now, we need to move past the autopsy of their failures and look at whether Alex Chriss (the new CEO) is actually fixing the engine or just polishing the chrome.

The next chapter

Are these structural issues or solvable problems? It’s the multi-billion-dollar question. This is why we call it the PayPal Problem. It’s probably a mix of both.

Now, I know many will get annoyed by this. It’s either fixable or it isn’t. But we can’t (and won’t) give you a black or white answer.

The Frankenstein tech stack and the lack of innovation velocity are solvable. Management is currently in the middle of a massive code cleanup, migrating to a unified platform to speed up product launches. We can see the results in things like Fastlane, which aims to bring one-click checkout to the unbranded world.

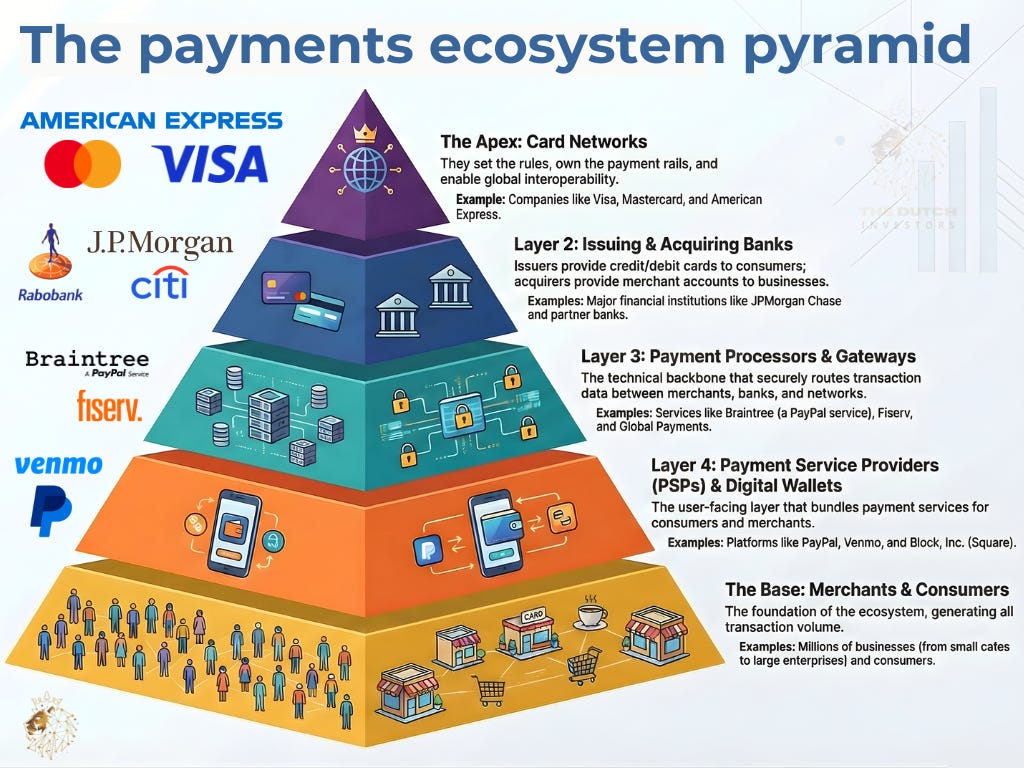

However, the structural issues are much thornier. PayPal is a layer 2 solution. It sits on top of mobile operating systems (Apple/Google) and on top of payment rails (Visa/Mastercard).

As long as Apple owns the NFC chip in your pocket, PayPal will always be disadvantaged in physical retail. Another massive issue is the payment rails. PayPal can’t magically stop paying Visa or Mastercard. Not just more volume, but better volume is what they need to fix their margins. It means they need people to use the PayPal button or Venmo.

What is needed to turn the tide?

For us to believe in a PayPal turnaround, we need to see three specific data points move in the right direction:

Transaction Margin Dollar (TM$) growth: Forget Total Payment Volume (TPV). It’s a useless metric if the margins are shrinking. We have to see the actual gross profit from transactions growing faster than the volume.

Fastlane adoption: If PayPal can prove that their new guest checkout (Fastlane) increases conversion rates for merchants by 10-15%, merchants will keep it. This is their best shot at fighting back against the Apple Pay friction advantage.

Venmo Monetization: Venmo is a crown jewel that has been underutilized for a decade. Transitioning it from a social splitting app to a pay-in-store and debit card ecosystem is essential for capturing the younger demographic they are losing.

We recently had a great conversation with Emir from Type-F Capital Equity Research, who knows all about PayPal. You can listen to the podcast on all platforms or read the article below.

Is PayPal Dead Money or Deeply Mispriced?!

We recently caught up with Emir from Type-F Capital Equity Research, who has just relocated to Japan, to discuss one of the most popular, or rather unpopular, stocks in the market: PayPal.

🎧 Listen on Spotify

🎧 Listen on Apple Podcasts

Our verdict

PayPal today sits in an uncomfortable middle ground. It’s no longer a clean, high-growth fintech story, but it’s also nowhere near the broken business some assume. What’s happening beneath the surface is a forced transition, not a choice, and the outcome is far from obvious.

Structural pressures are real. The payments stack is changing. Power dynamics are shifting. This is not a business on autopilot, and the next phase, the, call it PayPal 2.0 phase, won’t be quick or easy.

But as history shows, investors tend to overshoot, swinging from exuberance to excessive skepticism. That’s where asymmetry emerges, and with it, opportunity.

The downside case is widely understood and heavily debated. The upside case, however, requires a deeper look at incentives, unit economics, competitive positioning, and capital return mechanics that rarely make it into surface-level analysis.

To see exactly how we’re positioning around PayPal, including our full thesis, valuation, conclusions, and what we believe the market is missing, access the complete (38-page) deep dive and podcast, now available to TDI members on the TDI Dashboard.

"This $PYPL analysis is fascinating. It creates a real paradox: we have a company trading at a forward P/E of just 6.5x, yet the market just wiped out 20% of its value in a single day following the Feb 3rd earnings miss. It begs the question for beginner investors: Is this a 'value trap' where a cheap price hides a broken business, or is the market's reaction to the CEO transition and mid-single-digit guidance decline massively exaggerated? I'm actually using this exact PayPal 'Sunday Shock' scenario as a case study for my 'Noise Filter' series launching tomorrow. It's the perfect example of how to separate the 'Macro-Drama' from the actual 'Signal.' Would love to hear if you think Enrique Lores can reset the execution fast enough to justify this entry point! 🛡️📈"