Teqnion - Premium Research Report - Sneak Peek

Teqnion - Premium Research Report - Sneak Peek

Our fundamental analysis of Teqnion. An interesting Swedish serial acquirer operating in profitable niche markets.

“To offer leading products and specialist competence in market niches.”

Teqnion AB

This research report is a sneak peek of the entire fundamental analysis. If you want to read the entire research report, check out our premium reports.

In this sneak peek, we will dive into competitive advantages, risks, and opportunities.

Introduction

Business model

Competitive advantageManagement

Financial analysisRisks and opportunitiesValuationClosing thoughts

1) Introduction to Teqnion AB

Fall and rise

1.1 Introduction

In May 2023, Teqnion first came on my radar. Two months later, when I was reading the book 'The Outsiders' by author William Thorndike, it reminded me of one specific company: Teqnion. The book is about excellent CEOs and their characteristics. In my opinion, there are many similarities between the CEOs in the book and between CEO Johan Steene and deputy CEO Daniel Zhang.

We actually wrote a comprehensive summary on the book. You can check it out after reading this research report!

The company itself came onto my radar a few months earlier, after reading the book '100-baggers' by Chris Mayer. I decided to analyze Teqnion at the time and was so positive that I took a position in the company. Teqnion's past two quarters have been less than expected, and some skepticism has arisen about the company. As a result, the stock price has fallen somewhat and is now about 20% below the all-time high of February 2024. All in all, it was a good time to dive into this company again.

It's not surprising if you've never heard of Teqnion. The company is listed on the Swedish 'Nasdaq First North Growth Market' stock exchange in Stockholm. The company's revenue in 2023 was less than €150 million, which means we are dealing with a small-cap company. The current market capitalization is around €380 million. Disclaimer: I (Mathijs) own Teqnion shares since 2023.

1.2 History

Johan Steene, Jonas Häggqvist, and Erik Surén founded Teqnion in 2006. They obtained start-up financing through Jonas's parents and the owners of two small Swedish trading houses. The idea was to build a fast-growing industrial conglomerate. In the early years of Teqnion, everything went well, mainly due to a prosperous economy. At that time, according to Johan himself, Teqnion was 'naive' by not setting strict requirements for takeover candidates and not thinking much about the risks. The money that came in was invested in staff, offices, and companies.

Until the financial crisis arrived in the fall of 2008. With a weak balance sheet, Teqnion was hit hard. The income dried in just a few weeks, while cash continued to flow out of the company. Teqnion had to find a partner who could guarantee this, and found it in Paron Ventures. Many cost savings and reorganizations had to take place until mid-2009. After that, Teqnion was able to stand on its own two feet again, albeit with half the staff and turnover compared to a year earlier. After this, Jonas left the company and Johan remained as CEO. Here, he learned how to carry out takeover duties that Jonas had previously primarily handled. Logically, fewer acquisitions were made after almost going bankrupt during the financial crisis and because Johan Steene learned to take over companies himself. A turnaround took place here, because companies were better researched and a good strategy with strict criteria was developed. This mainly focused on finding 'boring companies in niche markets'. Later, we will return to the acquisitions that have been made so far, in order to recognize a pattern.

Teqnion's IPO took place in 2017, where it was listed on the 'Nasdaq First North Growth Market'. The IPO took place to raise additional capital and, therefore, increase the number of acquisitions.

Fast-forward to 2020. This is the year in which Daniel Zhang called Johan Steene for a conversation. The two agreed to have a drink and hit it off right away. Daniel Zhang was hired, almost on the spot, for a job at Teqnion as CXO (Chief Acquisition Officer). This is also one of the most important positions within the company, as Teqnion is a serial acquirer and turnover growth must therefore mainly come from acquired companies. In the management chapter, we will delve deeper into Daniel Zhang's background and why he is the right person for Teqnion in this position.

In 2022, Teqnion acquired its first non-Swedish company, Belle Coachwork Limited.

This is a company that focuses on building bodies for commercial vehicles, such as closed trailers for transporting cars. In the press release, Teqnion indicated that it expects to make the majority of future acquisitions in Sweden, but that it is also open to wonderful niche companies in other European countries. Enough history now; let's get to the revenue model!

2) Teqnion’s business model

The more boring, the better

2.1 The revenue model

As mentioned in the introduction, Teqnion is a serial acquirer from Sweden. In one sentence, Teqnion invests in profitable B2B companies that operate in niche markets and are easy to understand. CXO Daniel Zhang, in an interview with 'The Investors Podcast', gave a comparison with a “Two-engine growth machine”. He meant that Teqnion buys up profitable companies and can make new acquisitions with the profits from these companies. This allows Teqnion to grow both organically and through acquisitions, although Teqnion does not focus on fast-growing companies.

There are probably many criteria for Teqnion to take over a company. It is important to know what the selection procedure is, because it allows us to find out what distinguishes Teqnion from competitors. Here are a number of conditions that a takeover candidate must meet. In reality, this is, of course, more extensive.

The company operates in a niche market.

The company has built strong competitive advantages over the years.

The company is the market leader or almost the market leader.

The company is and will remain relevant in the future.

The company is profitable and has strong operating margins (EBITA above 9%).

The turnover of the candidate to be acquired is ideally between 20 and 150 Swedish Krona (SEK), which is approximately €2 and €13 million, respectively.

The return on the investment must be recouped within five years.

The company has a good and honest management team, with the founders or family ideally still involved in the company.

Teqnion never actually announces acquisition prices for companies. They say they do this partly out of a kind of courtesy towards the acquired candidate. If an owner sells his/her company to Teqnion, the whole world does not need to know what amount he or she received. Not disclosing takeover prices can also be a way to deceive competitors and have a better negotiating position compared to other candidates. On average, Teqnion acquires about 4 companies per year.

They have presented Teqnion's strategy as follows. In short: Teqnion acquires quality companies, which it then strategically supports and helps to further develop, resulting in strong margins being achieved, earnings per share doubling every five years and a healthy debt position. Why doesn't Teqnion just say: “We want to grow by 15% every year?” After all, this is the same as doubling every five years. This is because of Teqnion's long-term perspective. If you set an annual goal, you may make acquisitions in the final months of the year in order to achieve that 15% growth. Teqnion therefore wants to grow by 15% on average, taking the time to make good acquisitions.

Decentralized model

Teqnion works according to a decentralized model, while many competitors opt for central management of acquired parties. Subsidiaries, therefore, act independently and are allowed to make their own decisions. This enables companies to make faster, more flexible and more effective decisions in order to strengthen their competitive advantage. This says everything about the confidence Teqnion has in the parties they work with.

Teqnion works with so-called 'CEO coaches' who all have their own companies. They support the subsidiaries where necessary. When subsidiaries think they can reinvest money in their own company at a return of 15% or more, Teqnion encourages this. It is therefore not mandatory for acquired companies to transfer a fixed percentage of profits to the head office. Daniel Zhang stated in an interview with TIP (The Investors Podcast):

“If Teqnion would claim the cash flows and pull it to the HQ, our companies would lose their feeling of ownership. In the long-term, that’s negative.”

It is striking that Teqnion really allows the acquired companies to operate independently as much as possible. “They know the market, so they can make the best decisions,” is the idea. For example, Teqnion also promises not to relocate acquired companies and to be there for them in financially difficult times (more about this later when we delve into the sector).

CEOs of acquired companies are remunerated according to both a base salary and a variable part. This last part is a percentage of the increase in profits compared to the past three years. CEOs are thus motivated to make their own decisions about capital allocation. The management of subsidiaries does not need shares themselves in Teqnion to buy, but Daniel Zhang already indicated that this happens regularly. The companies that Teqnion is currently acquiring are mainly located in villages and small towns. As Teqnion grows, and therefore acquires larger companies, this may change. It is good to know that companies are located in villages, as there is more of a 'community' feeling here and companies want to be able to rely 100% on a company that takes them over.

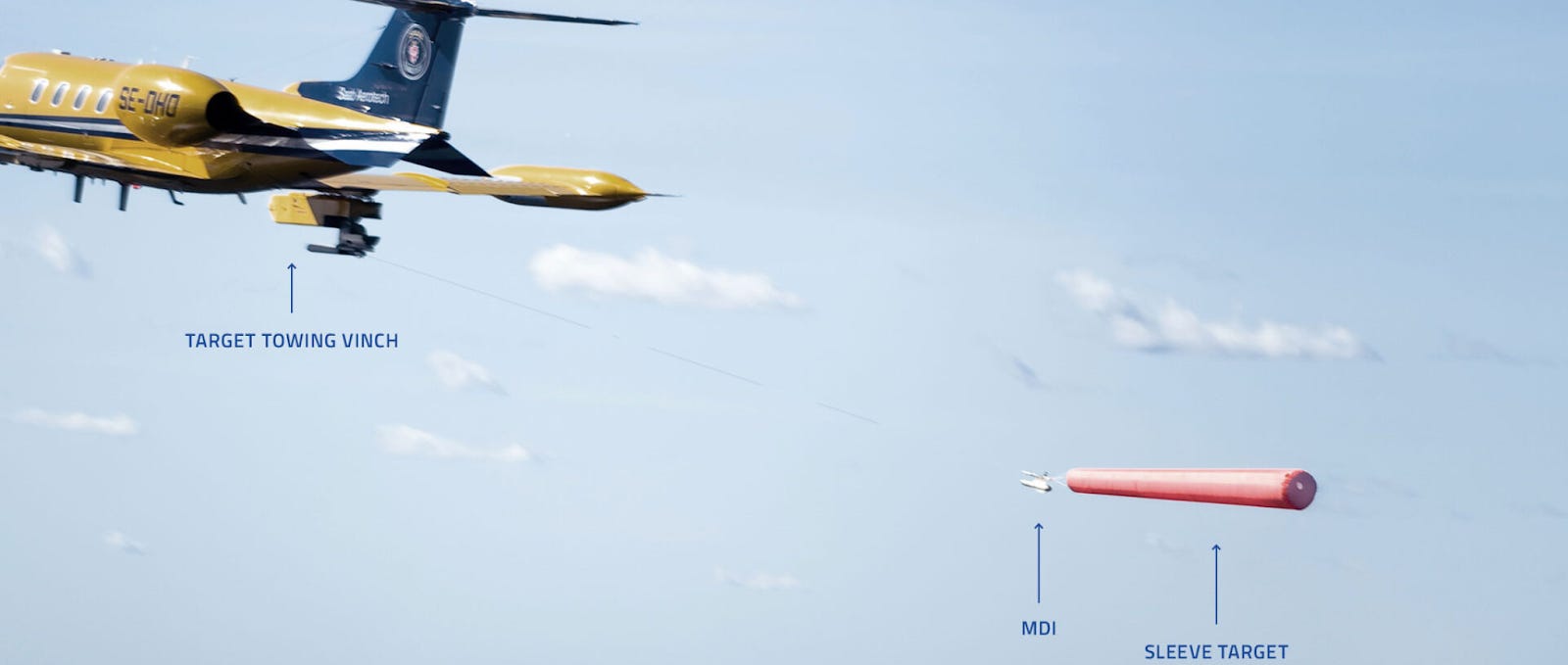

To get a feel for it: below is a Teqnion company that developed target indication systems for weapon systems. This is a big tailwind at the moment, given the increased defense spending worldwide.

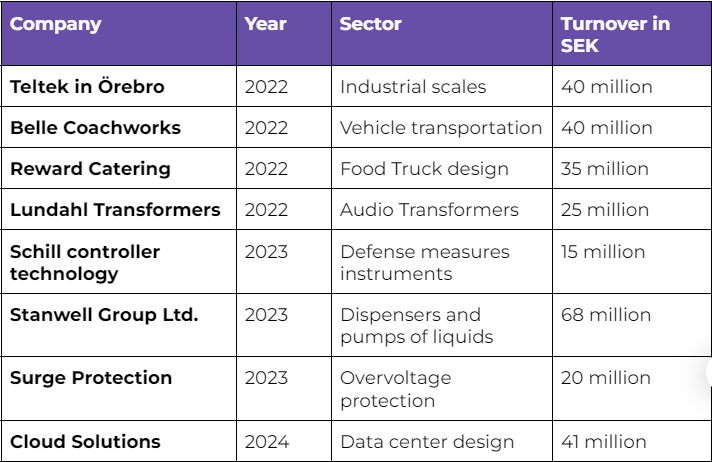

A selection of the acquired companies

Table 1 below shows Teqnion's acquired companies from 2022 onwards. It is immediately noticeable that Teqnion does not make major acquisitions, not even within their own set bandwidth. The largest acquisition in the past 2.5 years is of 68 million SEK, while Teqnion indicates that it sees up to 150 million SEK as a suitable acquisition size.

Teqnion's entire portfolio should be a “All Weather Portfolio”, according to Daniel Zhang. This means that different companies have different cycles and therefore keep the company in balance. Looking at Table 1, this does indeed seem to be the case. Defense, data centers, measuring instruments, dispensers and vehicle transport; quite diversified. Teqnion owns 100% of all their companies, except for the K-Fab company. Teqnion owns around 90% here, of which the former owner also has a share.

2.2 Sector & industry

At Teqnion, the main question is what makes this series of acquirers different from the many other series of acquirers, especially in the Swedish market. After all, it is difficult for us to plot the underlying companies in one sector, although we do take a moment to consider the Swedish housing market due to the current challenges and cyclicality.

A serial acquirer succeeds when it can reinvest generated cash flows in new companies for a long period of time at a high return. This is very important to monitor. If a serial acquirer can no longer reinvest, the growth strategy will collapse, and the company will probably not become a good investment. When companies in this market start paying dividends, they likely don't see enough opportunities to put their money to work efficiently. As a company grows, management is more likely to see fewer options to reinvest money in other companies or its own company. Consider, for example, Warren Buffett with Berkshire Hathaway. This business has become so huge that there are few options left. Yet Berkshire has not paid a dividend so far.

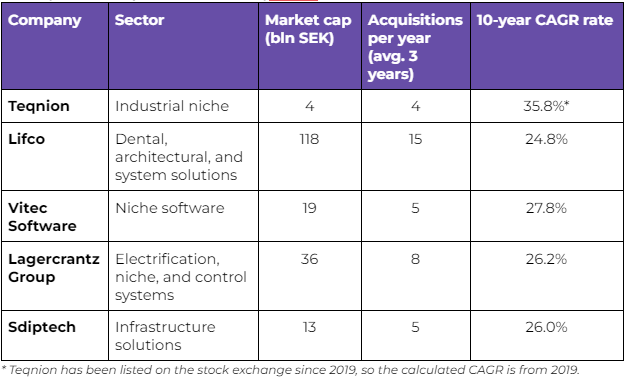

Below in Table 2 is an overview of a number of well-known and well-performing (looking at the stock price) Swedish acquirers. What is immediately striking is that they all deliver fantastic returns for shareholders. From the table below, we can also cautiously conclude that the larger a series acquirer becomes, the more acquisitions it makes. This seems logical, because to continue growing at a high pace, you have to make larger or more acquisitions over time.

What is also striking is that Teqnion is by far the smallest player with a market capitalization of 4 billion SEK. The possible growth path is therefore longer than with a Lifco. Companies simply cannot grow indefinitely.

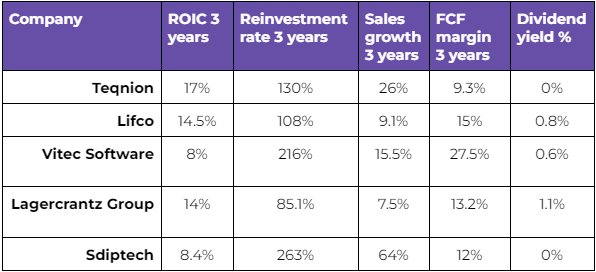

If we know what percentage of the free cash flow a company reinvests and what return it achieves on this, we can say something about the quality of capital allocation. Below in table 3, this data is displayed. All featured companies, except Lagercrantz Group, spent more on acquisitions than they brought in in free cash flow in the past three years. This does not have to be a problem, as long as shareholders are not extremely diluted by share issues and the debt position remains intact. This is still a question for the Sdiptech company. This company has a high reinvestment rate, but finances this with high debt and share issues; the number of outstanding shares has almost doubled in ten years.

If we look further at Table 2, we see that three companies pay dividends. Although Teqnion has 0%, the company has once paid a dividend. More about this later in the 'Capital Allocation' section. Three of the five series of acquirers below currently pay dividends. For Lagercrantz this can be explained at first glance, given that the reinvestment rate is below 100% and they therefore cannot (or cannot) reinvest all their cash flows. Things may be different at Vitec, as they spend almost twice as much money on acquisitions as they bring in. The question is whether paying dividends is the best option.

Industries Teqnion

The companies that Teqnion manages are located in various industrial niche markets. From the 2023 annual report:

“Within the Teqnion group we develop hydraulic tools, hoods and information signs for TMA vehicles. We manufacture chassis parts, high-voltage components and climate housings for data centers. We sell mounting materials, daytime running lights and measuring equipment transformers. We maintain gas turbines, refrigerators and pathological instruments.”

The versatility of the companies fits in with the desired “all-weather” portfolio, as mentioned earlier. However, Teqnion presented lower figures in the last quarter of 2023 and in the first quarter of 2024. Many investors were shocked and this led to a number of price drops. The reason for this was the weak performance of Teqnion's companies active in housing construction.

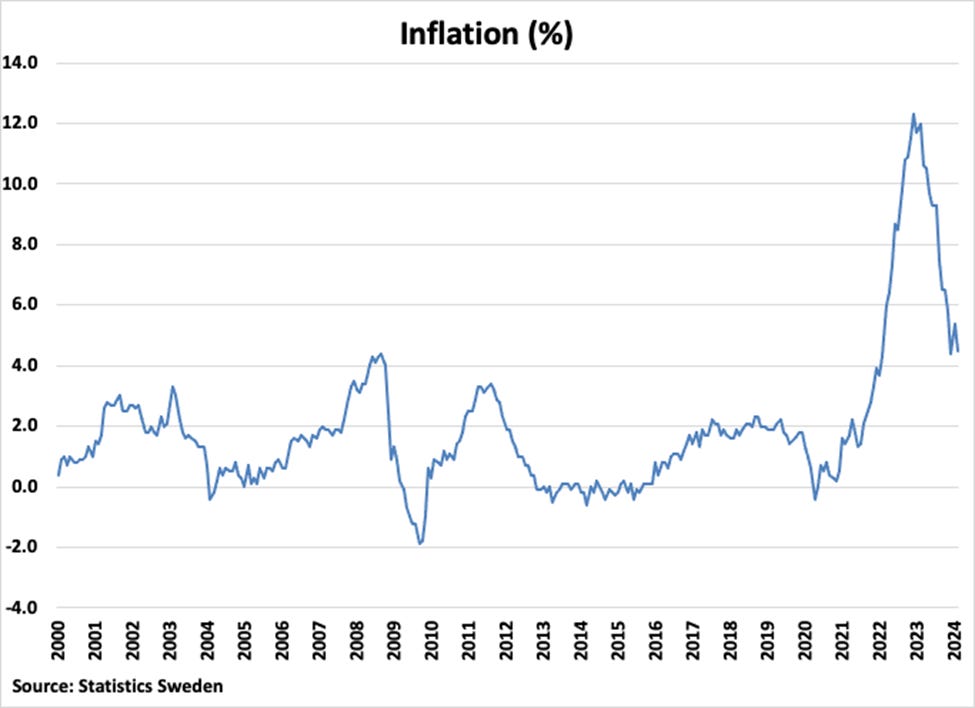

I don't want to dwell on it for too long, but I will still provide a brief explanation so that you know what the situation is. The biggest challenge in the Swedish construction sector is the rapidly rising interest rates. Partly due to rising inflation, the Swedish basic interest rate has risen from 0% at the beginning of 2022 to 4% in 2024. Households are therefore less likely to buy a new house and pay more to take out a mortgage. Teqnion has a number of companies active in housing construction; Grimstorps (wooden constructions), Hem1 (design villa architect) and K-Fab (furniture). Together, these companies account for approximately 8% of the book value.

I consider the chance that Teqnion will acquire more companies in this industry in the coming period to be small. This means that the weight of these three companies will only decrease in the coming years. In addition, you can also turn this short-term challenge into an opportunity; smaller players may collapse, expanding the market for the remaining companies. With Teqnion as a safety net, the aforementioned companies will not go bankrupt anytime soon. Inflation in Sweden has also weakened again in recent months, which could be a positive sign.

4) Management

Long term everywhere

4.1 CEO - Johan Steene

Between the lines, you have already been able to read something about Teqnion's management here and there. Two people will be discussed in this section: CEO and founder Johan Steene and CXO (Chief Acquisition Officer) Daniel Zhang. In my opinion, these two people are the most important for Teqnion because of their roles in the acquisition and acquisition capital allocation process.

He seems like someone who genuinely enjoys his work; During interviews, he laughs a lot and often mentions several times how much he enjoys his work. Although he has been actively involved with Teqnion for 17 years, he may be known in Sweden for something else. He is also an ultramarathon runner. In 2018, he set a bizarre record during the Big Dog's Backyard Ultra. He walked 455 kilometers here in about 68 hours. In any case, this shows an extreme amount of perseverance. If running 280 miles isn't a long-term prospect, I don't know what is. He also regularly runs back and forth to the Teqnion office, about twenty kilometers round trip.

You certainly won't find a photo of him in a three-piece suit. The culture within Teqnion is very informal. Even during interviews and important acquisition conversations, he just shows up in a t-shirt.

Steene has been focused on it since the early years of Teqnion controlling costs. Here are a number of examples that demonstrate this. While in LA for a trade show for a major subsidiary, Steene stayed overnight at a motel outside the city. The cheap options are always chosen; no expensive dinners, overnight stays, or flying business class. A second example is the investor call. Teqnion organizes this completely by itself, without a hosting party. You can ask questions live in Teams, via Twitter, or by email. The call in 2023 took place in a studio that they can use free of charge. During Q&As, Steene and Zhang usually appear at their own Teqnion office via a Teams conversation in which everyone can participate.

Then you might think: 'but he probably gets paid well.' You would be wrong. Johan Steene receives a basic salary of ‘just’ 1.5 million SEK ($141.000). He does not receive a fixed salary as a board member at Teqnion.

CFO - Daniel Zhang

Consider looking for companies with deep moats around them, the competence of management, and a focus on disruption-resistant companies with strong margins. Zhang even attended a Berkshire shareholder meeting in Omaha in 2023 together with CEO Steene.

After a number of detours with short adventures at McKinsey and Bain & Company, Daniel Zhang decided to send a message to Johan Steene for an appointment. From an early age, Zhang dreamed of building his own Berkshire, and saw Teqnion in the process. The appointment took place the next working day, and after the conversation, CEO Johan Steene immediately offered him a job. Zhang has now been employed since 2021.

I found out through the grapevine that he is the author of the book 'An Investment Thinking Toolbox'. In this, he discusses mental models while investing and how he has learned from mistakes. I think this is a very important quality of managers; admitting mistakes, reflecting on them and moving on. I see this not only with Daniel Zhang, but also with the aforementioned Johan Steene. During the Q&A of Q1 2024, I asked whether they had learned any lessons from the previous period with some setbacks. The answer from both was that they could have done more when all companies were doing well.

“Maybe another learning, there were times where we felt: maybe we should do something about this, because it's not going into the right direction, but the numbers are good. So a lesson is that we actually should do more during the good times as well."

It's nice that this is admitted.

4.2 Incentives

Normally, you have to dig through annual reports to find the remuneration policy. It is often difficult to understand and you have to deal with different reward structures. Teqnion is wonderfully simple in this. Teqnion's CEO, the other management team within the company and the CEOs of subsidiaries are all rewarded in the same way.

In addition to a fixed salary, there is a variable part. This variable part is 3% for CEO Steene in terms of the positive difference between the profit in the relevant year compared to the average profit of the past three years. So suppose Teqnion achieves SEK 100 million more net profit in 2025 than the average in the three previous years, Johan Steene would receive SEK 3 million. The remaining management team receives 0.6% of this difference. If you want to receive a variable bonus, you will have to increase your profit year on year.

CEOs of subsidiaries also share in the percentage profit increase of their company compared to the average over the past three years. Teqnion has not disclosed exactly what percentage this is.

4.3 Skin in the game

Johan Steene owns 861,471 shares in Teqnion. This amounts to a value of approximately 190 million SEK, or €17 million. Daniel Zhang owns 108,000 shares in Teqnion, amounting to a value of approximately 24 million SEK, or €2 million.

They are not the only two people within the company with a stock position. Teqnion shows this in every quarter through the slide below.

It is also striking that, in addition to CEO Johan Steene, many other management members also have a technical background. Combined with the fact that many of them have run or are still running businesses, this certainly helps them better understand industrial businesses and support subsidiaries.

Other shareholders

Erik Surén, co-founder of Teqnion, also owns 3.3% of the shares.

In addition, it is good to mention that Woodlock Capital, which Chris Mayer owns, has also built up a share position. It owns a total of 4.4% of Teqnion shares. Chris Mayer was also recently added to Teqnion's board of directors. Teqnion also has a number of other long-term investors committed from the early years, including Vixar AB since 2009 with 22.6% and Spiltan with 10.8%.

4.4 CFO changes

Teqnion has employed three different CFOs in the past three years. In this position, I like it when there is consistency within the organization, also considering the fact that errors can occur when work is transferred. New challenges and personal circumstances are the basis for the different departures. It is difficult to estimate whether it is a coincidence that three changes have been made in a short period of time. However, it is certainly a risk, which is also mentioned in the chapter on risks and opportunities.

Become a premium member and get access to the entire fundamental research report, including:

1- Introduction

1.1 Introduction

1.2 History

2- The company

2.1 The business model

2.2 Sector and industry

H3 - The competitive advantage

H4 - Management

4.1 Incentives

4.2 Skin in the game

4.3 CFO changes

H5 - The finances

5.1 Financial key figures

5.2 Capital allocation

5.3 ROIC

5.4 Financial objectives

H6 - Risks and opportunities

6.1 Opportunities

6.2 Risks

H7 - Valuation

7.1 Ratios compared to the past

7.2 Scenario analysis

H8 - Conclusion

very nice write up... Not that it may influence the thesis on Teqnion, but I wanted to quickly comment on Daniel's own stock picking history to show how he has picked some of the best companies in his personal portfolio: https://x.com/CXODanielZ/status/1684830521585463296. I somehow trust him as a stock picker and therefore as agood capital allocator.