Porsche AG - Research Report - Part 2

Porsche AG - Research Report - Part 2

Porsche's competitive edge

“Driven by Dreams”

Porsche AG

This research report is divided into three sections. This is Part 2 of 3. In this segment, we will explore:

The competitive advantage

The moat

Management

Dubble role

3) The competitive advantage

A unique brand

3.1 The moat

Porsche distinguishes itself as a car manufacturer based on a number of characteristics.

(1) Heritage. Sometimes a competitive advantage is difficult to demonstrate or explain. A company's heritage is one of those. Porsche has established a distinctive brand that is well-liked by consumers and auto enthusiasts, thanks to its history. The company has focused on designing and developing sports cars for more than 70 years. From the moment Porsche built its first real sports car in 1948, Porsche has been a luxurysports car brand with fantastic driving characteristics and the latest innovations. The stories that contribute to this history are almost endless. From the established records on the circuits of Le Mans, the past successes during Formula 1, the use of the cars inmost spectacular films and series, to popular celebrities who show off the brand.

When it comes to consumer brand loyalty, J.D. Power's consumer insights chose Porsche to be at the top in both 2022 and 2023. This was measured by calculating what percentage of car owners bought the same brand after trading in or selling their old car. Porsche comes out on top with 56.8% in America when it comes to premium cars.

In Germany, it is known that half of the people who bought a Porsche did so purely because of the Porsche brand. This is quite similar to the statistics as described in America. In many cases, once you own a Porsche, you don't want anything else. This is also evident from the 'churn rate' (the number of people who no longer had a Porsche at the end of 2023 who did have one at the beginning of 2023 / number of people who had a Porsche at the beginning of 2023) of less than 7%.

(2) Quality. The name Porsche breathes quality. As many as two-thirds of all Porsches ever sold since 1948 are still on the road. To me, this says two things: 1) A Porsche lasts a long time on average and 2) Porsche cars remain popular among car owners, regardless of the age of the car. You can, of course, also see this from how little a Porsche depreciates; some Porsches even become worth more money over time.

In this segment, quality is probably not the main reason for choosing a particular car; that is mainly the brand and the experience that someone has with a car.

Yes, some parts are shared within the Volkswagen Group. The Cayenne and Macan in particular share many parts with, for example, the Audi Q7, Volkswagen Touareq, and Bentley Bentayga. Consider software for the operating system, electrical components, and the type of steel used in different places. The critical components that influence driving behavior, such as the chassis, drivetrain, and engine, are developed per brand, so that each brand offers a unique driving experience. In the image below, from right to left: Porsche Cayenne, Lamborghini Urus, Audi Q7 and Bentley Bentayga. There are several similar parts in these cars.

This occurs to a lesser extent for the exclusive Porsche models. So far, Porsche has managed to find the balance well; Certain parts are exchanged without affecting the unique driving behavior and the different brands. However, Porsche and the VW Group should not go too far in exchanging parts, as this could affect the different brands. At this point it seems more of an advantage than a disadvantage; Porsche achieves cost benefits from this.

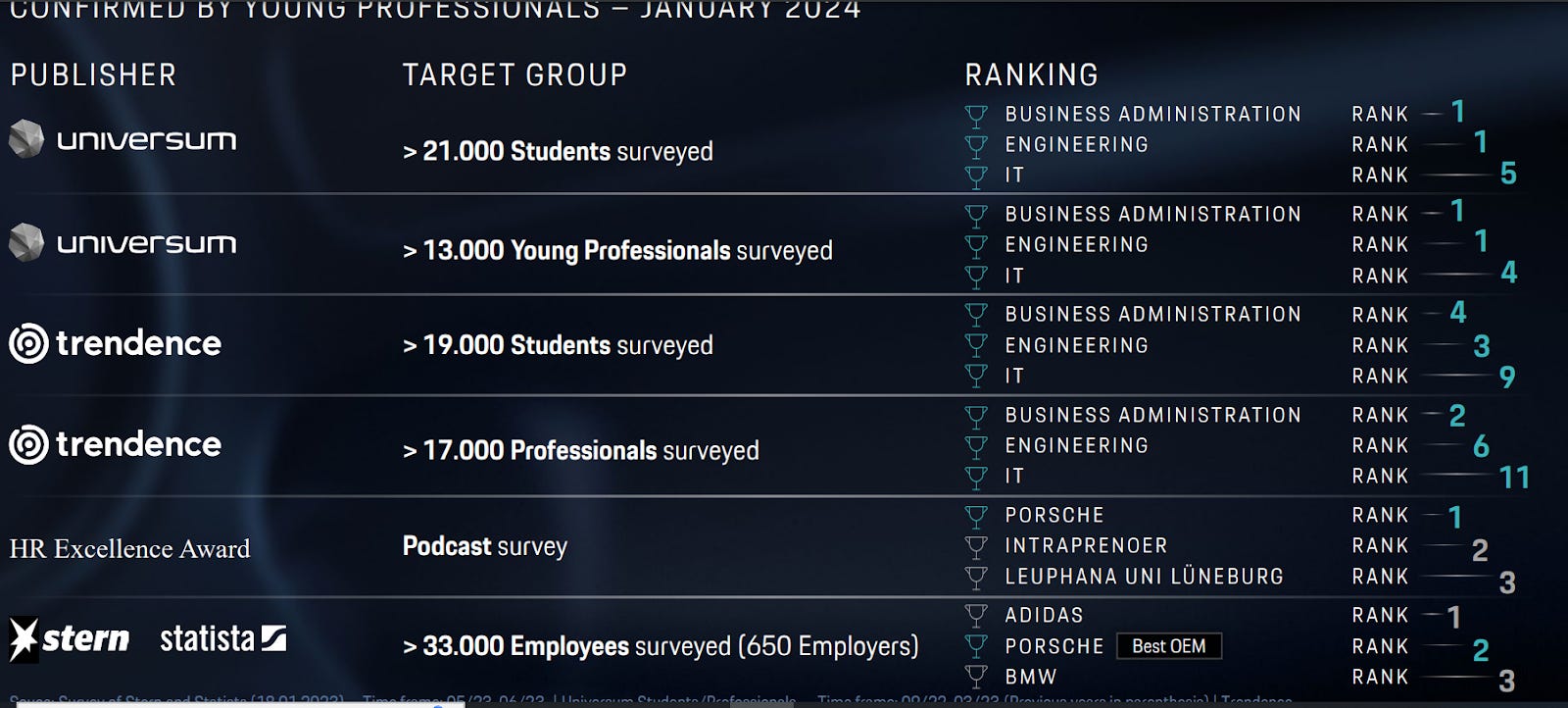

Quality and state of the art engineering also ensure that attracting talent becomes relatively easier. The studies below show that Porsche is seen as one of themost attractive employers among (student) engineers. This is important to continuously attract the best people. Porsche also appears to be one of the best among employees of various companies.

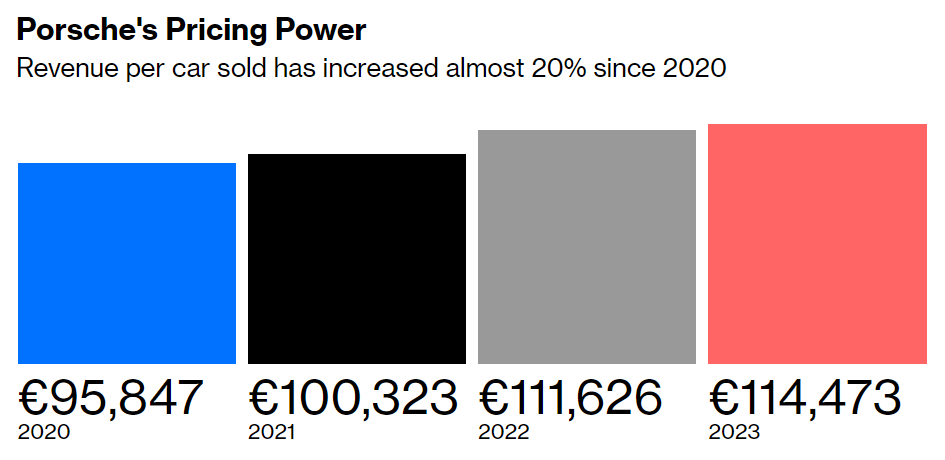

Below, you can see how Porsche has increased its prices in the last four years. This seems strong, but the same pattern can be seen throughout the automotive industry (apart from exceptions, such as Tesla lowering prices). Despite the fact that the increase is quite synchronous with the entire market, Porsche managed to increase its gross profit margin. This indicates that price increases exceeded inflation for Porsche.

The beautiful history and heritage that Porsche has built up over the years, together with the unparalleled quality of the cars, make for a very strong brand. Personally, I would argue that Porsche has a sustainable competitive advantage with its brand. The feeling and experience that people get when driving and purchasing a Porsche is special. You don't get this from a new Asian brand that started producing a few years ago. Porsche clearly does not compete with this. A strong brand has been built, and Porsche has done this successfully over the past 76 years. It still reaps the benefits of this today.

4) Management

The double role

4.1 About the team

The CEO of Porsche AG is Oliver Blume (left). He has been at the helm here since 2015. He started his career in 1994 at Audi, which is also part of the Volkswagen Group. He subsequently gained a lot of experience in production planning at the brands Audi, Seat and Volkswagen. From 2009 to 2013, he even held the position of head of production planning at Volkswagen. In 2013, Blume joined the Porsche board, where he became responsible for production and logistics.

It is remarkable that Blume not only runs the Porsche car brand. He has also been CEO of Volkswagen since 2022. There has been quite a bit of skepticism among investors about this dual role. As Volkswagen CEO, Blume would not be able to judge Porsche objectively and would therefore not make the right decisions. His response is that he walks away when decisions about Porsche have to be made on the Volkswagen board. Although it does not have to be a problem, the fact remains that Blume cannot focus with dozens of car brands under it.

Blume owns 31.101 shares of stock in addition to 2710 market-purchased shares. In total, this position has a (virtual) value of approximately €2.8 million. This amounts to 3.4 times his fixed basic salary.

Porsche's second man is called Lutz Meschke. In addition to serving as CFO for almost 9 years, he is also deputy CEO (co-CEO) of Porsche. Meschke has worked at Porsche since 2001 as VP Accounting, where he moved to the role of VP Controlling in 2004. Previously, he held positions at KPMG and Hugo Boss, among others.

Just like with CEO Blume, we also see a kind of duo role here. Since 2020, Meschke has also been a member of the management team of Porsche SE, where he is responsible for investments.

Meschke holds 24.805 (acquired) shares. The current value of this position is roughly €2.2 million This amounts to 2.3 times his fixed basic salary.

Looking at the entire management of Porsche, it is striking that most people have been working at Porsche for a long time, either within the holding company or in the Volkswagen Group. In addition, it is nice to mention that the Porsche family is still involved in the company. Wolfgang Porsche, the youngest son of Ferry Porsche, is Chairman of the Board of Commissioners. His brother Butzi Porsche designed the iconic 911. The great-grandson of founder Ferdinand Porsche is also still on the supervisory board. Given that the Porsche & Pich family still owns Porsche SE, Porsche is able to maintain a degree of family business status in this way.

Management compensation consists of three components.

Basic salary: (fixed amount paid out every month). This component is 30 to 45 percent of the total annual compensation package.

Short-term incentive (STI): can be seen as a bonus for achieving certain goals. These goals include the following

- Return on investment (weights 50%) - Target 24%

- Return on sales (weights 50%) - Target 15%

- ESG-targets (serves as a multiplier of the bonus based on the above two).

This component is 20 to 30 percent of the total annual remuneration package.Long-term incentive (LTI): Serves for the share price. Exists hereIt criteria for 100% from the EPS of Porsche AG. Shares acquired must be held for four years, where the reference price is compared to the average EPS and share price over those four years after which the shares can be converted into cash. This component is 30 to 45 percent of the total annual compensation package.

The base salary and the short-term incentive are paid in cash. The long-term incentive consists of virtual shares that can only be paid out after four years.

Part 3 is coming out tomorrow!