NIKE - Premium Research Report - Part 3

Our fundamental analysis of Nike. Just a 'shoe' brand, or much more? Is Nike a potential buy after its big -20% drop? Find out!

“Just do it!”

NIKE

This research report is divided into three sections. This is part 3 of 3.

Risks & opportunities

Nike’s biggest risks

Nike’s biggest opportunities

Valuation

Ratios compared to the past

Scenario analysis

Conclusion

Our verdict on Nike

6) Risks and opportunities

6.1 Risks

In its 2023 annual report, Nike stated that its three largest customers in the US account for approximately 22% of sales. The three largest customers outside the US accounted for 14% of turnover outside the US. If this percentage increases further, Nike will become increasingly dependent on these customers.

It's also important to monitor the success of Lululemon's shoes. Observe whether they catch on and take part of Nike's market or if they turn out to be flops.

Management has not been able to achieve their set goals for years. You should monitor whether John Donahoe and the rest of the management team will achieve the set goals in the future, admit their mistakes, and learn from them.

Pricing the shoes too high could cause customers to walk away, as Nike is not a luxury brand. It's essential to balance pricing to maintain customer loyalty while ensuring profitability.

6.2 Opportunities

There is still significant growth potential in the Chinese market. In FY 2023, only 15% of Nike's revenue came from China, compared to 44% from America. This is noteworthy given that 336 million people live in America, while 1.4 billion live in China—more than four times as many potential customers. Phil Knight highlighted the opportunity in the Chinese market with his statement:

"One billion people. Two. Billion. Feet."

Reaping the benefits of direct sales, now that they have invested in this for years and are now doing so less, can significantly increase profitability. By leveraging the established infrastructure and direct-to-consumer channels, Nike can enjoy higher margins and greater control over their customer relationships, which should positively impact their bottom line.

7) Valuation

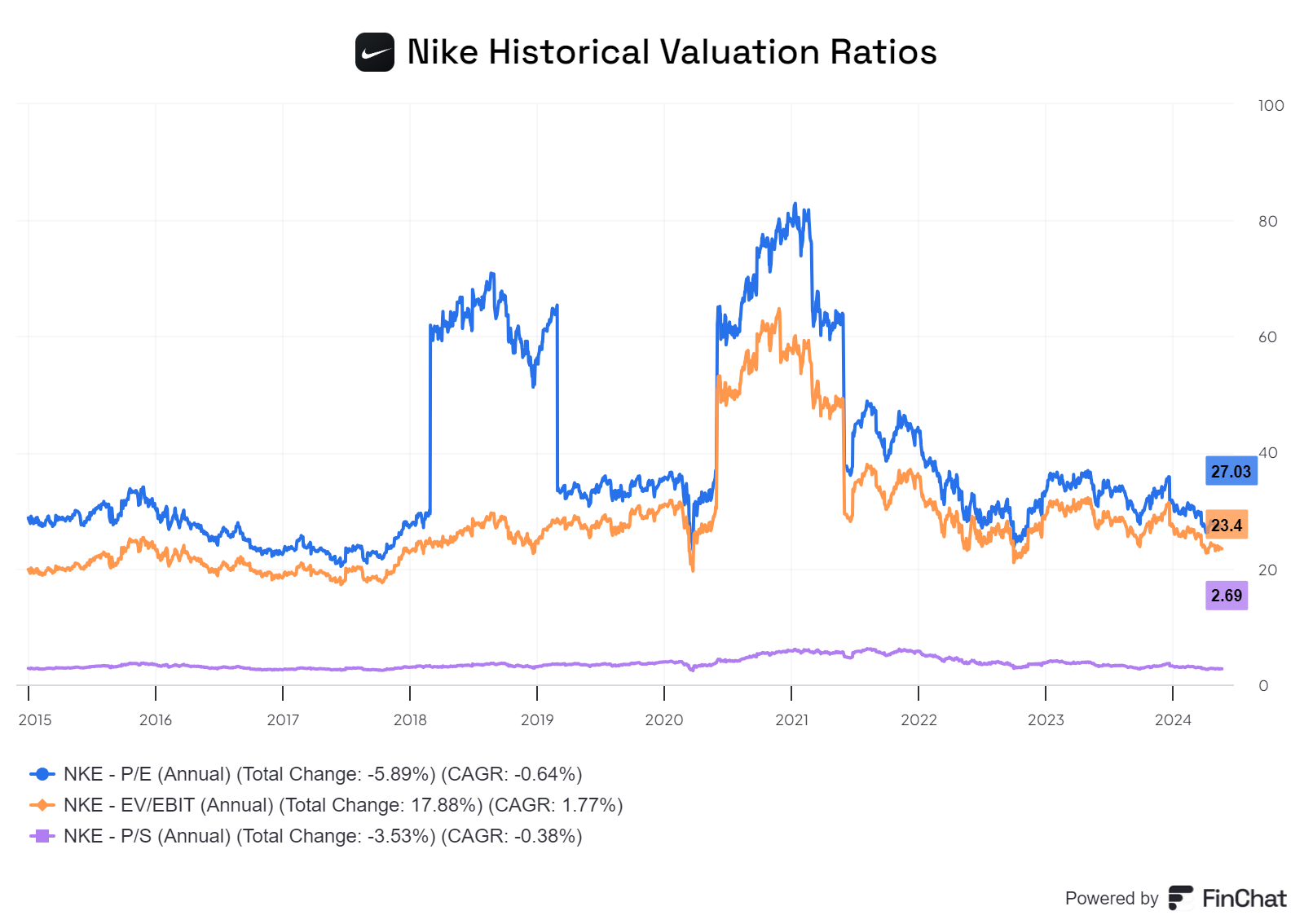

7.1 Ratios compared to the past

Nike is not valued expensively compared to the past. Below is the price/earnings ratio (blue), the enterprise value/EBIT (orange) and the price/sales ratio (purple) of the past 10 years.

7.2 Scenario Analysis

Normal scenario

Nike now trades at a price/earnings ratio of approximately 22, so profits must continue to grow to justify the current valuation. I expect profits to grow around 5% per year, which is slightly higher than world population growth plus inflation. In an optimistic scenario, where Nike prices its products higher and customers continue to buy, 10% profit growth per year is also quite possible, though I believe this chance is quite small.

FY 2023 earnings were $5.07 billion. If profits increase by 5% per year over the next 5 years, the profit in FY 2028 would be $6.47 billion, and by FY 2033, it would be $8.26 billion. Applying a price/earnings ratio of 20, this results in a market value of $165.2 billion in 2033. With the current market value at $138.2 billion, this gives a CAGR of approximately 2%. Adding 1.5% for share buybacks and 1.5% for dividends, the total CAGR would be around 5%, which is far below my hurdle rate.

Optimistic scenario

Suppose profits can grow 10% per year. In that case, profits in 2033 would be $13.15 billion. With an exit multiple of 20, the market value would be $263 billion, which translates to approximately a 10% return per year. With an exit multiple of 25, the market value would be $330 billion, yielding approximately a 12% return per year.

8) Conclusion on Nike

Nike is a great company with a strong brand name. It is a company defined by its story rather than just its numbers. The brand must remain cool and popular with the crowd. It is difficult to distinguish oneself in the shoe and clothing industry, where there is little that sets casual and premium clothing apart from competitors. Nike operates in the premium segment and has a strong brand name, but beyond this, it does not have a strong moat. The success of the company and the share price depend heavily on the strong brand name, making the company very vulnerable.

The management is adequate, and the valuation is reasonable, but nothing about this company truly stands out to me. Even with the significant drop in the stock price, I do not find this company interesting enough to buy.