Hims' moat in the making

This company is sharing scale advantages with customers

Although Hims, a U.S.-based leader in telehealth solutions, is only seven years old, we believe the company is already showing signs of building one of the strongest types of moats: scale advantages shared.

Moats usually take time to develop. Building a great business model demands years of effort and resilience. Rome was not built in a day, and neither are most businesses.

Investing in companies without a moat is risky. A fragile business model makes it easier for competitors to outsmart you or price you out of the market. On the other hand, investing in companies that are building a moat can offer great opportunities for patient and long-term investors.

In this article, we will explore how Hims is working to achieve scale advantages, and how it gives those advantages back to customers through a better platform and lower prices. But first, what does Hims actually do?

Hims’ business model

Hims is U.S.-based telehealth company that has been growing with a 95% CAGR since 2018. It is active in the categories dermatology, mental health, weight loss and sexual health.

Hims makes use of recurring subscriptions, where customers can purchase treatment plans for their specific conditions. 85% of customers that are on the platform for at least two years, stay customer. Also, their retention rate for GLP-1 medications are significantly better than the industry-average.

The company is market leader in their respective categories, while they are rapidly expanding their product portfolio, revenue and profit. They’ve gained market share in an impressive way, as can be seen in the picture below. What is Hims’ secret?

Scale advantages (shared)

Hims operates its own medicine production facilities and develops its own medications. Because of Hims’ large and growing customer base, these costs can be spread out on more and more customers. Hims is the largest consumer telehealth company and thus benefits here. Advertising plays a crucial role here as well. Now that Hims has grown significantly, each ad impression shown to potential customers is more valuable than it used to be.

Not all U.S. states currently permit telehealth services, but as more states legalize and support it, the impact of national campaigns, like the Super Bowl commercial, increases dramatically. The broader the reach of telehealth, the more effective and profitable these large-scale ads become.

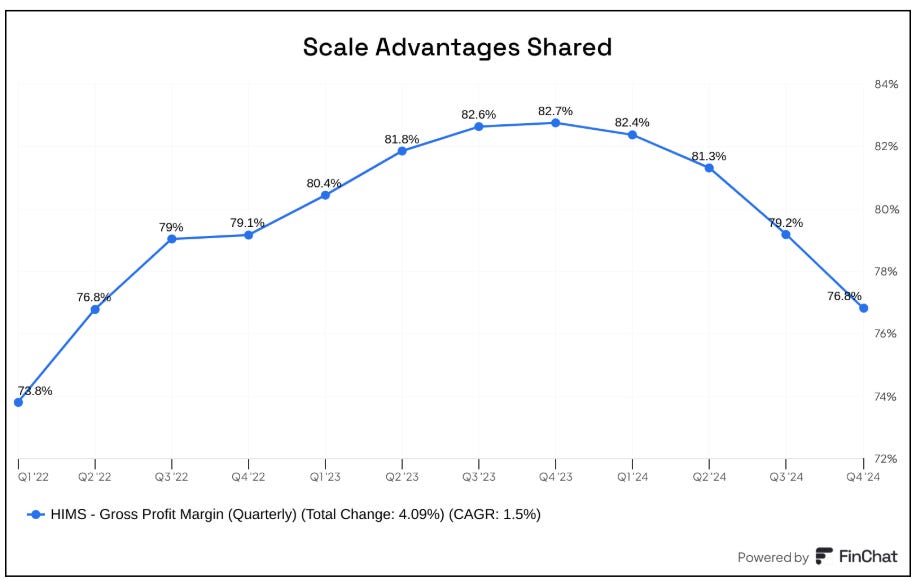

In fact, Hims’ target is to have gross margins in the mid 70% range, which is lower compared to this moment. It is because Hims shares (marketing) cost advantages with their customers. As CFO Okupe explained during the Q4 earnings call:

“Line of sight to future operational efficiencies gave us comfort to make our injectable offering even more affordable. We reduced the price for our 12-month SKU from $199 to $165 per month in December.”

In this graph, you can see how Hims is voluntarily lowering its gross profit margin.

CEO Dudum told this about the broader strategy during that same earnings call:

“Our ambition will always be to scale quickly, negotiate either through our own third-party partners or through the verticalization of our own infrastructure to be able to then bring that price down over the coming year and bring it to people in a way that ultimately delivers great outcomes.”

Hims must demonstrate that it can consistently share its success with customers over the long term. If the company manages to maintain this balance, it has the potential to become an unstoppable force. While it took Rome more than 800 years to reach its full glory, we may be able to draw even more reliable conclusions about Hims’ future within just a few years.

Final Thoughts

The worlds’ greatest companies do not have only one competitive advantage; they have multiple. In our latest premium analysis about Hims, we share more information about what makes Hims a (potential) fantastic company and what moats it is developing.

While there are certainly many positive aspects to Hims' business model, we have also outlined the associated risks that investors should consider.

Hims could be the first of many analyses you receive from us, just join TDI-Premium by clicking the button below.

Special thanks to Ray Myers (X.com) from Global Equity Briefing for joining the Hims & Hers audio analysis. Ray and Mathijs dive deep on what makes Hims such a compelling thesis.

Have a wonderful day and happy investing.

The Dutch Investors.

Reminds me Teladoc..