Heico Corp: On track to become a 1000-bagger

Why has Heico Corp. been such a great investment?

Since the Mendelson family started managing Heico Corporation in 1990, the company has delivered a staggering 86,000% return for investors. We know that it’s hard to find 100-baggers, but this company is on its way to become a 1000-bagger. The question is: “What enabled this company to deliver these stellar returns for investors?”

In this article, we’ll break down what sets Heico Corp. apart from its competitors.

Understanding Heico Corp.

Heico is a serial acquirer that was founded in 1957. From the 1990s, the company started a new strategy of buying companies in two segments, led by the Mendelson Family who still manage the company.

The business is roughly divided into two segments:

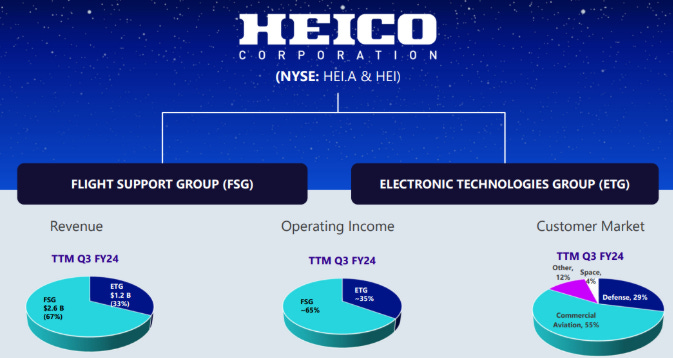

Flight Support Group (FSG)

Electronic Technologies Group (ETG).

While the first group is responsible for the largest portion of revenues (67%), the second group realizes higher operating margins.

In the FSG division, Heico is involved in developing and producing PMA’s (Parts Manufacturer Approvals) for the aviation-, aerospace- and defense industry. It is also involved in MRO (Maintenance, Repair & Overhaul) activities and takes care of spare part distribution. Among major customers are airlines such as American Airlines, Fly Emirates and RyanAir as well as the U.S. Department of Defense.

In the ETG division, Heico operates dozens of niche companies that create electric components for a variety of industries. Some examples of products here are power distribution systems and capacitors. What sets Heico apart here is that its products are capable of operating under the harshest circumstances (defense, aviation, healthcare etc.).

All right, all right. You probably have many questions right now. Let’s explore why Heico has been so succesful in what it’s doing.

4 Reasons for Heico’s success

Lowest cost provider

Heico offers products that are typically 30–40% cheaper than those produced by OEMs (Original Equipment Manufacturers). The more units Heico sells of a particular PMA, the faster they recover the associated development costs. To pass these savings on to their customers, Heico lowers prices when they anticipate higher sales or once those sales materialize. This strategy not only shares their cost advantages but also strengthens customer loyalty and satisfaction. As a result, Heico's products can sometimes be up to 50% more affordable than those of their OEM competitors. That’s an absolute no-brainer for many airlines.Smooth and successful PMA process

If you're unfamiliar with a PMA: it stands for Parts Manufacturer Approval. It refers to a product that can legally be sold as a replacement part for the 'original' one produced by an OEM. Obtaining a PMA requires approval from the FAA, which is a process that's an art in itself. It involves complex procedures where companies must thoroughly prove their parts meet strict quality and safety standards.

Heico has built a strong relationship with the FAA, earning a reputation as one of the most reliable players in the industry. The company has a flawless safety record of zero accidents. The company now holds over 20,000 PMAs, while its closest competitor in the US has just 2,000. That should tell you something about Heico’s market leading position.

PMA’s owned by Heico’s subsidiary Wencor Incentive alignment between subsidiaries, employees, management and shareholders

The Mendelson family is a master in creating an ownership mindset throughout the organization. To illustrate that with some examples:More than 400 Heico employees own more than $8 million of Heico stock in their 401K account.

The management of acquired company always keeps a substantial part of the business (usually 10-20%) to keep them highly involved with the company.

Heico employees own more than 2% of total shares outstanding, this is excluding the Mendelson members, who are drowned in Heico stock.

Acquisition discipline

As a serial acquirer, one of the most crucial factors is making high-quality acquisitions at the right price. Heico excels in this by seizing opportunities during industry downturns when valuations are most attractive. They remain disciplined, staying within their core business segments and avoiding speculative "moonshot" investments. The companies they acquire consistently generate strong cash flows and hold dominant positions in their niche markets. Heico’s price performance and underlying financials reflect their outstanding capital allocation strategy. Here are some key examples, which we’ve highlighted in our premium analysis:

Interesting to know more about Heico’s great subsidiaries and its acquisition strategy?

→ You can read the Heico Corp. analysis now as a premium TDI Premium member

Feel free to join the 100+ members to enjoy weekly in-depth stock analyses like Heico Corp.

Have a wonderful day and happy investing.

The Dutch Investors.